Commodities - A Relay Race (Lap 2)

Lap 1 done, Lap 2 in progress

Relay race - a team event with four players in each team, where each member in the team completes a lap (of same length) and passes on the baton to the next team member. To finish the whole event all four members have to finish the race before their competitors.

We believe, we have something similar on our hand in commodity markets with only difference being different Lap sizes.

Lap 1: Prices move up shortages go unnoticed (No noise)

Lap 2: Prices continue higher but supply response is slow (Early noise of Policy response)

Lap 3: Capex and Price moves in tandem (Start of industry response)

Lap 4: Excess investment (Industry moves ahead of itself)

Lap 2 Hypothesis with “China” as a Noise factor:

Lap 1 and Lap 2 as mentioned above, have many similarities in terms of price and supply patterns, but the differentiating factor is ‘Noise’. Yes, in Lap 1 most things happen silently, but as the action continues noise levels start to increase.

In latest, “China” has come out with proposals to standardize how commodity price indices are constructed - this can be a good step in terms of transparency but will it lead to any price correction? Probably not, unless one believes the consumers are hoarding inventories (in fact the opposite is true as supply chain impacted globally).

Rather, any artificial suppression in prices could further delay the supply response leading to steep commodities prices in times ahead.

Goldman Sachs agrees with us that “China” is more noise this time as it is no longer a marginal buyer of commodities. Implication, “China is no more commodity price setter”.

Goldman sees, commodities as a combination of reflation trade as well as inflation hedge, and we agree that it sounds logical at this point. Snippets from Seeking alpha highlight the target price from Goldman for Oil and Copper.

Commodity Prices - Why we think there is more upside before supply catches up?

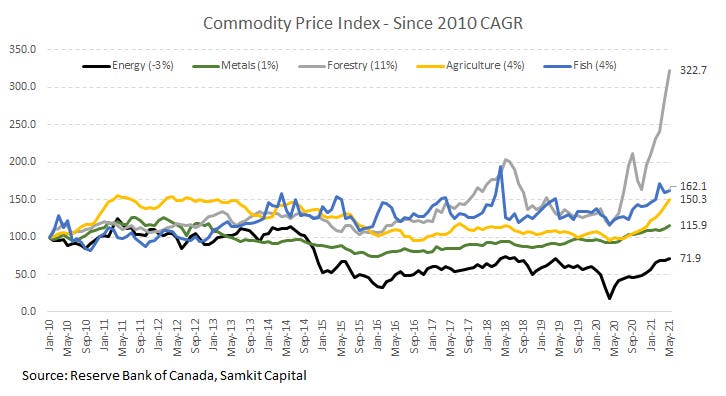

Below chart from Reserve bank of Canada shows an interesting picture, since 2010 soft commodities have higher CAGR growth rates vs metals and energy. If we adjust for average global annual inflation (from World bank) 2.6%, Energy and Metal prices have degrown over last decade.

Energy and Metals are below 2010 levels adjusting for World CPI inflation, will energy go back to 2010 levels may be not but the real prices could track general commodity basket. For metals to reach 2010 levels, ~23% of price hike is required from levels seen in May-21. (Implied 23% growth for Oil will be ~$90/ barrel).

These prices are important as that will incentivize suppliers to increase supply into the market. So in our opinion more upside to prices is left in Lap 2 before supply starts to come onstream.

Capex to pickup but will remain concentrated in “Green” Zone:

Capex for miners have remained cyclical last peak was seen in 2012 when capex peaked at $140bn, with iron ore contributing a large chunk of capex. Post 2012 a secular decline in capex will 2016 led to mini commodity boom in that period.

Currently capex has peaked in 2019 and is expected to gradually decline till 2022 to levels of $60bn. Given the data is pre-pandemic weak 2020 and robust 2021/22 may change things on capex side. So, we may see gradual uptick in capex spends (Chart from Mckinsey).

ESG Financing: will lead to capex concentration in “Green” metals

ESG will shift global capex financing to green metals like copper, nickel and cobalt and in turn increasing hurdle rates for Oil and other metals.

Valuation implications (from McKinsey)

Strong correlations mean we need to get price forecasts right in order to make money in commodity stocks. Therefore, supply side response becomes even more important and right now where we stand, supply side risk remain low and price trajectory for most commodities is expected remain upward. Therefore, any correction in prices of metal stocks is more of a buying opportunity.